Why one-size health benefits don’t cut it

How employees use health care, and their costs, varies by individual. Explore the implications on employer benefit design when sliced by generation.

- Costs are rising across all generations — Baby Boomers make up just 12.9% of the workforce, but drive more than 20% of costs.1

- Each generation has unique health risks — Gen X peaks in chronic disease spend, Millennials' chronic condition rates jumped from 44% to 47% in one year, and Gen Z ER visits rose 5.2% while primary care use remained low.1

- Flexible benefits are a retention imperative — 68% of employees rank health insurance as a top retention benefit, making personalized, choice-based plans essential for a multigenerational workforce.2

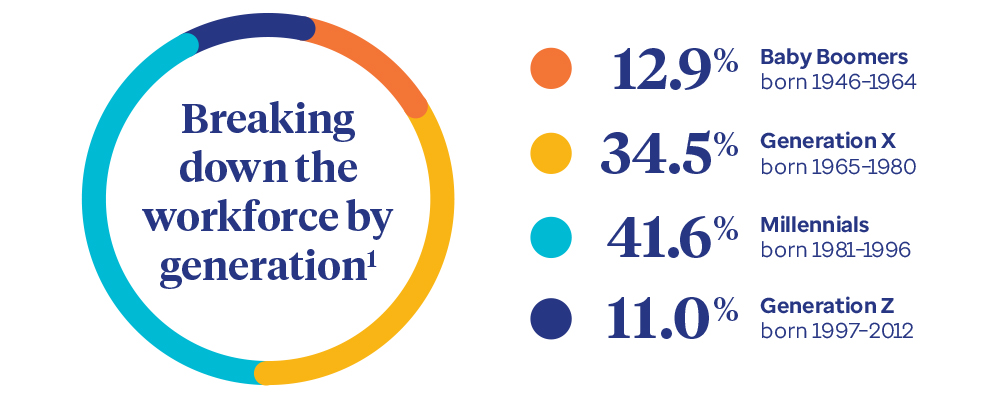

From new college hires to seasoned executives, it’s not uncommon for an employee population to span multiple generations. In fact, there are 4 commonly defined generations currently active in the workplace today: Baby Boomers, Generation X (Gen X), Millennials and Generation Z (Gen Z).

With these multigenerational employee populations come varying health care needs, expectations and preferences. For instance, Baby Boomers tend to have different health care concerns and priorities than their younger counterparts based on several factors, including age, life experience and socioeconomic influences.

This can make it challenging for employers to determine which health care experiences are the right fit for their unique employee populations — and finding the right fit matters.

Why? Sixty-eight percent of surveyed employees prioritized health insurance as a key retention benefit,2 and robust benefits can often lead to higher overall employee satisfaction and better employee experiences. That's why it’s important for employers to understand their employee population’s needs and keep generational preferences in mind when designing their benefit strategies.

Tailored benefits for a multigenerational workforce

UnitedHealthcare supports every life stage through a broad yet thoughtful portfolio of benefits, programs and digital tools — each designed to bridge generational disparities and meet the distinct needs of today’s diverse workforce.

This resource explores how UnitedHealthcare benefits and digital tools can be aligned to the unique needs of each generation, helping employers build a health plan strategy that works for their entire workforce.

Breaking down the generational divides and cost implications of today’s workforce

Findings from the UnitedHealthcare 2026 Health Trends Report reveal a consistent and consequential trend: Health care costs rose across every generation currently represented in the workforce from 2024 to 2025.1

- Baby Boomers: Costs climbed by 10.9%

- Generation X: Costs climbed by 13.7%

- Millennials: Costs climbed by 12.8%

- Generation Z: Costs climbed by 11.7%

This cross-generational increase underscores a critical imperative for employers, brokers and consultants to move beyond one-size-fits-all benefit strategies and develop approaches that account for the distinct health needs, priorities and behaviors of each generational cohort. By meeting each group where they are and engaging them in meaningful, relevant ways, there’s a real opportunity to drive the kind of behavior change that leads to smarter utilization of the health system and of the benefits made available to them.

Baby Boomers — 62–80 years old by the end of 2026

Employees are working longer than they once did: The average retirement age has risen from 57 to 62 in just a couple decades — a meaningful shift that reflects financial pressure and increased longevity.3 In fact, nearly half of surveyed Baby Boomers aren’t confident they have enough income to last through retirement or indicated they won’t be able to retire.4 Part of this is due to Social Security benefits not starting until age 62 — with full benefits not kicking in until age 67 to 705 — and Medicare not being available until age 65.3 At the same time, life expectancy continues to rise for both men and women.

This poses a problem for employers, because the longer this generation remains in the workforce, the more costs they incur. For instance, despite representing around 13% of UnitedHealthcare members in 2025, Baby Boomers drove more than 20% of the total costs to employers. Additionally, the average per-member, per-month costs by generation surpassed Gen X by 1.6 times and Millennials by 2.5 times, according to the UnitedHealthcare 2026 Health Trends Report. This is largely due to the more complex health needs that come with age — which often lead to more medical care and, ultimately, higher costs.

In care settings, Baby Boomers tend to prefer more traditional care pathways than other generations, favoring in-person visits when scheduling appointments compared to Millennials and Gen Z members, who choose virtual visits 2.5 times more often than Baby Boomers and Gen Xers.6 They also generally follow and rely on provider advice and care more than any later generation — and often make more optimal health care decisions.1

Generation X — 46–61 years old by the end of 2026

Retirement security is also a growing concern for Gen Xers. Nearly half report they must push back their retirement timeline due to insufficient savings, and only 38% feel confident they will retire on their original schedule7 — a financial reality that closely mirrors the pressures facing Baby Boomers.

Compounding that strain, many Gen Xers find themselves navigating the demands of the “Sandwich Generation” — simultaneously caring for their children and aging parents or family members.8 Alongside Millennials, Gen X bears a disproportionate share of this responsibility, consistent with the fact that 1 in 4 Americans now serve as caregivers.9

These pressures coincide with rising health care costs tied to chronic conditions. UnitedHealthcare data shows that employer spend on cancer, circulatory conditions and digestive disorders peaks among employees in the 50–59 age group.1 As a result, Gen Xers account for approximately 35.5% of total employer spend — a striking figure given that Millennials represent a larger share of UnitedHealthcare commercial membership.1

The convergence of physical health challenges with significant career and caregiving responsibilities may also be taking a toll on mental health. Yet utilization data reveals a persistent gap: Gen Xers are not fully accessing the behavioral health benefits available to them.10

Care preferences for this cohort tell a nuanced story. While Gen Xers tend to favor in-person care, members ages 30 to 49 — spanning both Millennials and Gen X — accounted for the highest share of virtual care users over the past year, representing more than 40% of all virtual visits.11 Gen Xers are also more willing than their older counterparts to switch providers in pursuit of improved health outcomes.12

Millennials — 30–45 years old by the end of 2026

Currently the largest segment of today’s workforce, Millennials may stay in the workforce for longer than previous generations since they (along with Gen X and Baby Boomers) also have higher levels of retirement insecurity.13 In addition to longer lifespans, Millennials may be carrying more student debt than other generations.13

As Millennials head into their 40s, they typically experience more health challenges. The share of Millennial members considered “well” declined from 25% to 22% between 2023–2024 and 2024–2025, while those living with chronic conditions rose from 44% to 47% and those managing complex conditions increased from 6% to 7%.11 This generation, particularly ages 30–34, are having the most births and are responsible for the majority of maternity-related claims and costs.14

According to UnitedHealthcare data, Millennials experience the highest prevalence of behavioral health conditions, with women experiencing them more than men.1 This may be due to grappling with big life changes, such as caring for children and aging parents. As part of the “Sandwich Generation,” they’re open to professional support and self-care resources that fit their potentially busy schedules and tight budgets.10

As this generation came of age with social media, they are among the least likely to rely on traditional health care with about 51% visiting a provider less than once a year.12 They are also quick to adopt health-related technology.12 Because of busy lives, they typically want care that is convenient and effective — both for themselves and those in their care. Despite that, this generation visited the ER more frequently than any other generation and, along with others, have decreased their utilization of virtual care.1

Generation Z — 14–29 years old by the end of 2026

Technology and social media have been a part of Gen Z lives since the very beginning, which is why they may turn to family and friends, social media and even AI for medical or health advice.15 Only half of Gen Z respondents trust hospital systems and doctors, compared with 64% of the overall population surveyed.16 This generation also demonstrates a notably higher adoption of digital wellness apps and telehealth programs, and they are 50% more likely than Gen Xers or Baby Boomers to report using digital mental health resources.16

When it comes to utilization patterns, Gen Z members showed particularly concerning patterns, relying more heavily on expensive ER services while being the least likely generation to use primary care.1 In fact, their ER utilization increased 5.2% from 2024 to 2025, according to UnitedHealthcare data.1 Gen Z (along with Millennials) saw the largest spending increases between 2023 and 2025 across both catastrophic and non-catastrophic claims.

It’s also important for employers to help manage burnout among this generation. When it comes to behavioral health, Millennials and Gen Z members have a 61% higher rate of utilization compared to their Baby Boomer and Gen X counterparts.6 Nearly half of Gen Zers say they feel stressed or anxious at work all or most of the time.17 And Gen Z women tend to seek care for behavioral health issues more than men, having 2 times the claims for anxiety and depression.6

Designing a health care experience for a multigenerational workforce

With Millennials dominating today’s workforce, employers might be tempted to cater to that generation’s preferences. But that approach has the potential to alienate other generations, who are just as important to their employee population. Employers should instead design their health plan and benefits around the diverse needs of a multigenerational workforce based on its specific makeup.

1. Leverage data and analytics to inform benefits strategies

Working with a carrier that possesses robust data and analytical capabilities is essential for employers seeking to drive meaningful health outcomes across their workforce. By leveraging these insights, employers can be better positioned to identify where the greatest health disparities exist, target areas of opportunity with precision and tailor outreach strategies that foster deeper engagement and more equitable care.

2. Help employees find quality care

Research consistently shows that engaged members generate lower health care spend across generations.11 Both digital experience and advocacy programs play important roles in helping employees understand their health plan, navigate the health system and take full advantage of their benefits. Carriers that are continually enhancing these capabilities can make it easier for members to make more informed care choices that can also improve plan satisfaction. This may include offering a provider search experience that prioritizes results based on cost criteria, coverage and other personal preferences, or delivering personalized, real-time support through AI-powered capabilities like Avery (UnitedHealthcare’s AI companion) or Advocates who can help connect members to care and resources based on their individual needs.

3. Offer employees ways to help engage and manage their benefits

Today's employees across virtually every generation expect a connected, digital-first benefits experience,18 making it more important than ever for employers to select a carrier that offers a single, simplified point of entry into all available benefits. UnitedHealthcare delivers that through an integrated ecosystem of offerings accessible to members through the UnitedHealthcare® app and myuhc.com®. There, members can do everything from search for care and enroll in relevant programs based on their benefits and coverage to track and pay claims. By removing some of the confusion around navigating benefits and care, employers may end up with employees who are healthier and more satisfied with their employer-sponsored benefits package.

4. Help empower employees with more choice and control over their offerings

Today's workforce is more diverse than ever, and a one-size-fits-all approach may leave many employees without the support that may be most meaningful to them — making customizable, voluntary benefit options a critical tool for employers looking to meet their team members where they are. By empowering employees with offerings they can select — or even purchase using employer-funded dollars — based on individual needs, employers can deliver broader, more personalized and scalable benefits packages that employees may value.

For instance, UHC Store gives eligible members access to an exclusive digital shop where they can purchase a variety of well-being offerings. UHC Store can accommodate various employer-contribution and consumer payment models, including lifestyle spending accounts (LSAs), health savings accounts (HSAs), flexible spending accounts (FSAs) and more — to help give employers flexibility in how they support employees and empower choice. For example, self-funded employers can choose to fund an LSA that works with UHC Store to help offset employee costs for a range of LSA-eligible offerings. Putting employees in the driver’s seat may help employers better meet the diverse needs and preferences of a multigenerational workforce.

5. Support whole-person health needs

Focusing on just the medical side of an employee’s health doesn’t offer a complete picture. Taking a whole-person approach means addressing one’s physical, mental, financial and overall health and well-being needs. In fact, 95% of surveyed employers believe that offering benefits that support overall well-being can enhance the health care experience for employees and make their benefits package more attractive to them.19 An employee’s care may also be better coordinated when benefits and programs are integrated under a single carrier rather than fragmented across different vendors and carriers. Designing a benefits package that accounts for all the factors that may influence an employee’s health can help ensure every generation of a workforce feels supported.

Share

Share